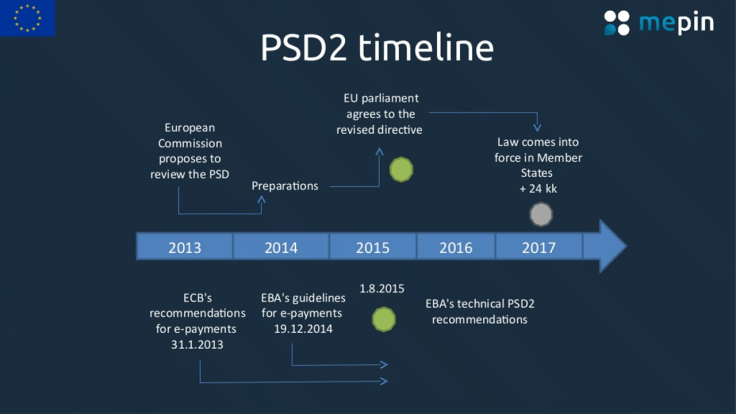

As January 2018 inches closer, financial institutions and fintech startups across Europe have PSD2 on their minds. The legislation introduced by the European Commission is set to open consumer financial data to third-party providers through APIs, creating both opportunities and hurdles in the financial ecosystem.

Not only is PSD2 a major step towards Open Banking and a unified European financial market, but it is priming the stage for innovation in Europe like never before. Global investments in fintech have increased more than tenfold the last five years and are estimated to exceed $150 billion in the next 3–5 years. The possibilities for innovation and process improvement in the wake of PSD2 signify increased market opportunities, consumer choice within the ecosystem and competition among businesses and banks for customer acquisition and loyalty.

Nevertheless, the directive’s unspecific language coupled with changing attitudes about technology have prevented truly reliable predictions of what will result from PSD2 when it comes to the financial market. Possible scenarios for Europe in the wake of PSD2 include a free, open market; an open, domestic market; maintenance of the status quo; or big banks dominating after build solutions from their data before it becomes available to others (known as the “first mover advantage”).

While it’s uncertain how startups and banks will ultimately fare or collaborate and how their interaction will impact the European financial services landscape, one thing is clear: PSD2 is sparking innovation and new market opportunities in Europe.

Opportunities for innovation from banks

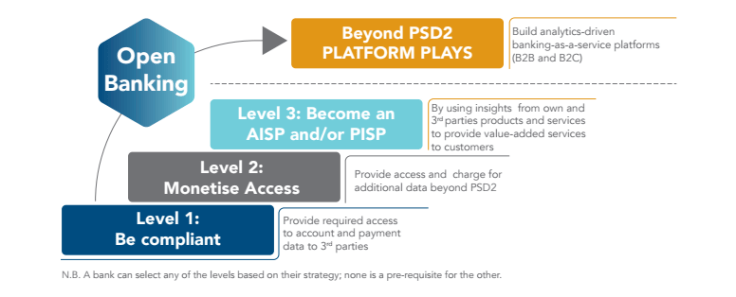

PSD2 poses unique challenges for banks, who must not only bear the majority of IT infrastructure costs related to open banking standards, but also carefully monitor customer data being shared for the first time with third parties. 68% of banks feel they will be weakened as a result of PSD2. For banks to succeed moving forward, they must shift away from the view of PSD2 as a threat or simply an exercise in compliance, and move toward driving innovation.

“PSD2 provides banks with a unique opportunity, should they choose to exploit it,” says Kanika Hope, Strategic Business Development Director of Retail and Corporate Banking for Swiss software company Temenos Group. “In order to protect themselves from the risk of disintermediation, banks should respond to the directive by not merely complying, but by exploiting the directive to create new business models aimed at creating new and deeper relationships with customers and at generating new revenue streams.”

These topics recently served as a springboard for conversation in Luxembourg at an intimate conference titled Mastering Transformation: PSD2 and Open Banking. Jointly hosted by The LHoFT Foundation and Temenos Group, the evening spurred discussion on the future role of banks, how they can prepare for and take advantage of PSD2, and how they might collaborate with fintech startups.

The Mastering Transformation conference not only touched on the challenges banks face, but also shed light on their advantageous position. Open banking fosters improved identity verification and authentication, and could lead to seamless onboarding and increased customer acquisition if banks pay attention to best practices in user experience design.

“We need this regulation to convince banks that the ‘party is over’ and to work for customer loyalty and profit. That being said, banks deserve our loyalty too, as they pay the price for regulation and security that we all desire,” says Conny Dorrestijn, Board Advisory Member of Holland FinTech. “If banks treat fintech companies as their new clients who bring them more clients, they are very well positioned to win.”

Some banks, such as ING and Danske Bank, are choosing to build up in-house innovation teams to ensure a first-mover advantage. Others, such as Danish bank Saxo, are voluntarily opening up APIs to welcome external innovation. Still others prefer an external collaboration and community approach; Nordea, for example, hosts accelerator programs and works with startups on process improvements. The idea behind this approach is that banks can keep a finger on the pulse of innovation while continuing to do what they do best.

One particularly interesting anomaly involves payment app Swish, which is currently the no. 1 fintech app in Sweden, built by a consortium of Nordic financial institutions. Their collaboration created a payment product that is now rivaling Swedish payment unicorns such as Klarna and iZettle.

Most commonly, banks are acquiring or partnering with third-party fintech players to begin offering Value Added Services enabled by open APIs. One such bank is Banque Internationale à Luxembourg. Even major non-finance corporations such as IBM are recognizing the opportunity in partnering with banks.

A certain benefit of PSD2: Innovation from non-bank tech companies

Whether it’s collaborating with banks or competing against them, non-bank fintech companies are seizing an increasing share of the financial services market and creating new markets through innovation. PSD2 will only accelerate these companies’ abilities to utilize consumer data.

All-mobile banks

Mobile solutions such as Atom Bank, N26, Fidor and Figo have begun taking their share of the market, providing agile and responsive customer experiences that differentiate them from the slow-moving traditional banking services. Consumer trust and uptake of these solutions is at an all-time high (N26 tripled its user base within a year to 300,000 across Europe) and the increasingly open market offered by PSD2 will undoubtedly spark more offerings in all-mobile banking.

Not only are all-mobile banks paving the way in their own right, but they are also in prime positions to link up with other startups to help optimize customer experience. Global fintech expert Elizabeth Lumley believes these kinds of partnerships will create the quickest impact after PSD2.

“I think there is going to be major change, it’s just going to be more challenging and take longer than people think,” says Lumley. “So if I was a fintech startup and I was given the choice next year of hooking on to Starling — a bank that is built on embracing APIs — or HSBC, I’d pick Starling. HSBC would be my long term goal since they are the biggest bank in the world, but with Starling it would be easier and quicker to make an impact.”

Regtech

Navigating compliance legislation and generating revenue from PSD2 are no easy feat, which is why fintech companies are creating solutions to simplify these processes. In the realm of finance, regtech companies cater to everything from cybersecurity to KYC.

Swiss company Temenos Group, a participant in the Mastering Transformation conference, is perhaps one of Europe’s best examples of pioneering regtech as a leading provider of software for banks.

Luxembourg, a country with its finger on the pulse of European financial regulations and innovation, is a pioneering region for regtech. One example is Governance.io, a risk and compliance solution for investment fund professionals that is embodying the shift towards Know Your Customer (KYC) independent of country-specific markets. The company’s CEO, Bert Boerman, says, “We are already collaborating across borders as our different solutions are in many cases very complementary and together deliver real solutions to the customer’s many challenges.”’

Aggregators, recommenders & personal finance

European fintech companies are beginning to develop customer-driven solutions for aggregating financial data, recommendations, and personal finance management — much like what Mint has been doing in the U.S. for years.

Germany’s Treefin uses APIs to offer customers single-dashboard views of their investments, insurance policies, and bank accounts. London startup TrueLayer is paving the way for fintech companies to more easily access bank APIs. According to co-founder Francesco Simoneschi, the company is building a simple, secure and universal API to take advantage of “the full scope of opportunities enabled by PSD2 and Open Banking.”

Mutaz Qubbaj, CEO of personal budgeting app Squirrel, says that PSD2 will help his company move past a reliance on outdated screen-scraping as a means of opening up personal finance information. “PSD2 can only work towards bringing even more control and value to our community,” he says.

Insurtech

Open access to account data brings opportunities for customer services based on analysis of consumer spending habits. Collaboration between banks and insurtech companies is becoming increasingly common; BBVA has invested in both Hixme and Hippo, solidifying the link between financial data and insurance in new business.

Meaghan Johnson, Director of Research at digital banking research platform 11:FS, says some banks are already utilizing smart insurance techniques for their customers. “In Sweden we have seen a few banks start to send push notifications offering travel insurance when a customer is at an airport, ferry, or train station.”

Payments

The area of payments is one in which we are seeing moves towards a unified European market where cross-border e-commerce and transactions are both enabled and encouraged. A study from PwC found that 88% of respondents already use third-party digital payment services, such as PayPal and Sofort, and 85% rate their trust in these solutions as high or very high.

Klarna, Transferwise, iZettle, and Adyen are some of Europe’s biggest names in innovative payments. In Luxembourg, payment companies Digicash, PayCash and Olkypay are leading the market and growing steadily.

Looking forward

The enactment of PSD2 signals more than just an immediate change for the financial landscape; it’s one further step toward a consumer-driven economy in which technology plays a leading role. 2018 will reveal how traditional financial institutions react and evolve to the changing landscape, and how new players rise to the challenge of satisfying market demands.

Leave a comment